Available 24 hours / 7 Days a Week

Email: info@senftlegal.com

Facing the stress of a car accident injury can be overwhelming, especially when it comes to the potential cost from medical bills, vehicle repairs, and even missed days of work. One of the reasons car insurance is required in virtually every state is to help to relieve this burden. However, not all state insurance systems are equal, a fact perhaps made clearest by the divide between at fault and no-fault states. Understanding the difference between at fault vs. no-fault states—and what they mean individually—is crucial to knowing how to respond to an accident, and what kinds of compensation you can expect.

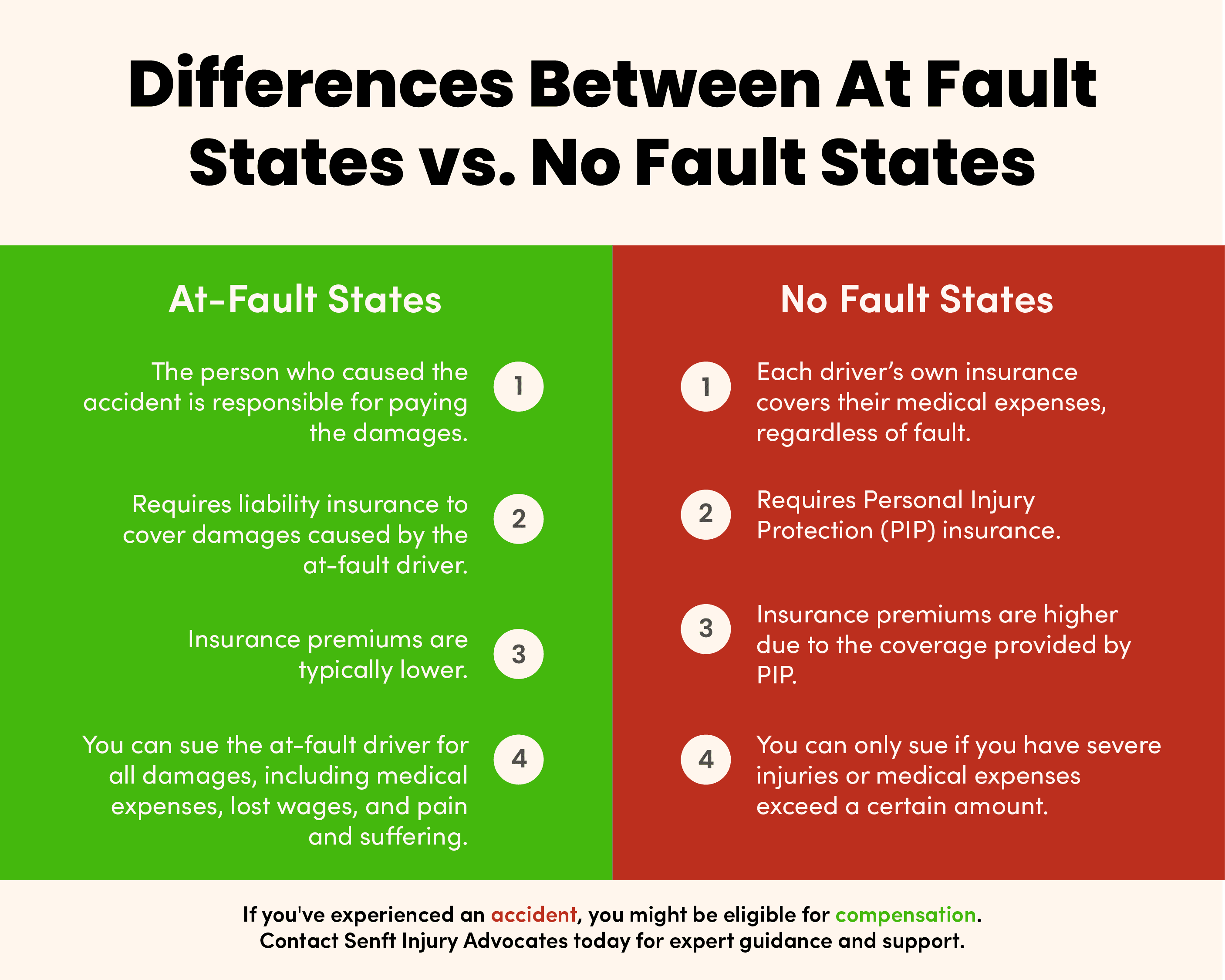

An at-fault state is essentially one in which fault the at-fault driver pays for damages. When an auto accident results in injury or damage to person or property, these states determine an at-fault party to assign financial responsibility.

38 states, as well as the District of Columbia, follow an at-fault system.

In order to ensure that an at-fault system can be upheld, at-fault states require drivers to carry liability insurance. Since auto accident damages can easily outstrip what an at-fault driver might be able to pay out of their own pocket, liability insurance not only provides a critical safety net to financially responsible drivers, but also helps ensure that victims have access to financial recovery, one of the most basic fundamentals of insurance in the U.S.

When you’re injured in a car accident in an at-fault state, you can file a claim with the at-fault party’s insurance. However, it is important to know that some insurance companies may be uncooperative or try to invalidate your case in order to reduce the amount they have to pay. An auto accident attorney can help you negotiate for the full amount you deserve, even taking the matter to court if necessary.

Fault can be better understood through negligence, a critical concept of tort law. Negligence occurs when one party fails to uphold a duty of care—a legal expectation to avoid causing harm to another person—leading to injury.

This may seem like a clear indicator of fault, but in many cases, multiple parties can be guilty of negligence. When this happens, determining how much compensation is owed gets trickier.

There are a few types of negligence systems in place to determine fault and compensation, which vary from state to state. Understanding the distinctions between these negligence systems is crucial. Here’s a quick breakdown:

A no fault state is one where the at-fault party is not necessarily held financially responsible for car accident injuries. Instead, personal injury protection (PIP) insurance typically pays for injuries in a car accident. Unlike liability insurance, personal injury protection covers the policyholder for injuries incurred in an accident. That means if someone hits you in a car accident and you need compensation for your injuries, you’ll generally turn to your own insurance, rather than the other party.

The following 12 states fall under a no fault system:

In no-fault states, drivers must have personal injury protection. PIP generally covers medical expenses, lost earnings, and other non-reimbursed costs, known as economic damages, regardless of fault. The exception to this is vehicle repairs, which are typically not covered.

In addition to PIP insurance, no fault states still usually require liability insurance, which means that premiums may be higher on average.

Yes, someone can still be held at fault for an auto accident in a no fault state. They’re called “no fault” states because they bypass the need to determine an at-fault party before compensating a victim for their injuries, potentially allowing for a simpler claims process and faster recovery. However, this does not absolve the at-fault party of blame, and in some cases, they can still be held partially responsible for your compensation.

As a general rule, in no fault states your first source of compensation for car accident injuries and other economic damages is your own PIP insurance. However, in some cases, you can still obtain compensation from the at-fault party, even in a no fault state.

For example, there are some types of accident damage that PIP insurance does not typically cover, such as vehicle damage, or non-economic damages— losses that don’t have an inherent monetary value, such as pain and suffering, wrongful death, or reduced quality of life. If you suffer significant damages outside of the scope of your PIP insurance, you may be able to pursue further compensation from the at-fault party.

You can also typically sue the at-fault party for compensation if the damage you sustained in the accident exceed your state’s set verbal or monetary threshold.

System | States Where It May Apply | Insurance Requirements | How Compensation Works |

|---|---|---|---|

At-Fault | Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, District of Columbia, Georgia, Idaho, Illinois, Indiana, Iowa, Kentucky*, Louisiana, Maine, Maryland, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey*, New Mexico, North Carolina, Ohio, Oklahoma, Oregon, Pennsylvania*, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming | Liability insurance typically required, with varying minimums for damage caused to other persons and their property. Other types of insurance may or may not be required, depending on state legislation. Generally, this can result in lower required premiums, but it may lead to longer claims processes as it places more financial strain on insurers. | Damages are typically paid to the victim through the at-fault party’s liability insurance. This includes medical bills, lost wages, property damage, pain and suffering, and more. |

No-Fault | Florida, Hawaii, Kansas, Kentucky*, Massachusetts, Michigan, Minnesota, New Jersey*, New York, North Dakota, Pennsylvania*, Utah | Both liability insurance and personal injury protection are required. Other types of insurance may or may not be required, depending on state legislation. Generally, this can result in higher required premiums, but it can lead to simpler, shorter claim resolution for accident victims. | Compensation can come from different sources depending on the type and the severity of the accident. Economic damages for personal injury such as medical bills and lost wages can be obtained through your own PIP insurance. Further damages, such as property damage or pain and suffering, may be obtainable through the at-fault party’s liability insurance. Potential recovery may depend on whether injuries are deemed serious enough, depending on the state’s threshold. |

*"Choice" no-fault states, including Kentucky, New Jersey, and Pennsylvania, allow drivers to choose between an at fault or no-fault insurance policy, meaning both systems can be relevant in these states.

Even with a fundamental understanding of at-fault vs. no-fault states, navigating your unique situation to secure the full compensation you deserve is no easy task. You may have to work around unclear deadlines, uncooperative insurance companies, tricky legal intricacies, and more. Fortunately, you don’t have to face this alone.

At Senft Legal we understand that navigating the complexities of fault, negligence, and compensation after a car accident can be overwhelming. Our car accident attorneys are ready and willing to support you in maximizing your potential recovery. Contact us today, and let us advocate for your rights, guide you through the legal process, and work to secure the compensation you deserve.